一、交易策略解释

核心思想

Keltner Channel策略是一种基于通道突破的趋势跟踪系统,核心思想是在价格突破由均线和波动率构成的通道时进行交易, 该策略基于市场的趋势行为和价格回归特性,认为价格突破通道边界后,如果有趋势确认,则很可能会继续向突破方向运行,形成显著的价格移动; 而当价格回归到通道中线或突破反向通道边界时,意味着趋势可能已经结束,应当及时平仓。

理论基础

Keltner Channel由Chester W. Keltner于20世纪60年代首次提出,后经Linda Bradford Raschke改进完善。其理论基础主要包含以下几个方面:

波动率适应理论:市场波动率不是恒定的,而是周期性变化的。Keltner Channel通过ATR动态调整通道宽度,使策略能够适应不同的市场环境。

突破持续性:根据道氏理论和动量原理,价格突破重要技术位置后往往会有延续性,特别是在趋势确认的情况下。

均值回归原理:价格在大幅偏离均值后,往往会有回归均值的趋势,这也是策略中使用EMA作为通道中线和平仓依据的理论支持。

策略适用场景

趋势明显的市场:黄金、原油等大宗商品在宏观经济变化或地缘政治事件影响下,往往形成持续的趋势行情,是该策略的理想应用场景。

波动率适中的市场:波动率既不过低导致无法突破,也不过高导致频繁虚假突破的市场环境最适合该策略。

流动性充足的品种:流动性好的产品滑点小,有利于策略的精确执行。

策略原理

核心指标计算:

- Keltner Channel上下轨: 通过动态ATR乘数调整通道宽度,使策略能适应不同的市场环境。

dynamic_multiplier = ATR_MULTIPLIER if trend_strength > 0.5: # 强趋势时使用更窄的通道 dynamic_multiplier = ATR_MULTIPLIER * 0.8 upper_band = ema + dynamic_multiplier * atr lower_band = ema - dynamic_multiplier * atr- EMA(指数移动平均线): 作为Keltner Channel的中轨,EMA比SMA反应更快速,能更好地跟踪价格变化。

ema = pd.Series(close).ewm(span=EMA_PERIOD, adjust=False).mean().values- ATR(真实波幅): 用于测量市场波动率,是通道宽度的决定因素。

tr = np.maximum(high - low, np.maximum( np.abs(high - np.roll(close, 1)), np.abs(low - np.roll(close, 1)) )) atr = pd.Series(tr).rolling(ATR_PERIOD).mean().values- 趋势确认: 使用短期EMA与主EMA的交叉确认趋势方向,降低虚假突破风险。

trend_direction = 1 if ema_short[-1] > ema[-1] else -1 if ema_short[-1] < ema[-1] else 0 trend_strength = abs(ema_short[-1] - ema[-1]) / close[-1] * 100 # 趋势强度百分比- 动态止损设置: 基于ATR设置初始止损,并根据价格走势进行移动止损调整。

# 初始止损 stop_loss = current_price * (1 - STOP_LOSS_PCT * current_atr / current_price) # 多头止损 # 移动止损 if TRAILING_STOP and high_since_entry > entry_price: trailing_stop = high_since_entry * (1 - STOP_LOSS_PCT * current_atr / current_price) stop_loss = max(stop_loss, trailing_stop)交易逻辑

开仓信号:

- 多头开仓:价格突破上轨道且短期EMA位于长期EMA之上(趋势向上)

if current_price > current_upper and trend_direction > 0: # 开多头逻辑- 空头开仓:价格跌破下轨道且短期EMA位于长期EMA之下(趋势向下)

elif current_price < current_lower and trend_direction < 0: # 开空头逻辑平仓信号:

- 多头平仓:满足以下任一条件时平仓:

- 触及止损位

- 价格跌破通道中线(EMA)

- 价格跌破下轨且趋势转为向下

if (current_price <= stop_loss or current_price <= current_ema or (current_price < current_lower and trend_direction < 0)): # 平多头逻辑- 空头平仓:满足以下任一条件时平仓:

- 触及止损位

- 价格突破通道中线(EMA)

- 价格突破上轨且趋势转为向上

if (current_price >= stop_loss or current_price >= current_ema or (current_price > current_upper and trend_direction > 0)): # 平空头逻辑- 风险管理:

- 动态止损:初始止损基于入场价格和当前ATR设置

- 移动止损:随着价格向有利方向移动,止损线也相应调整,锁定部分利润

- 趋势过滤:使用短期EMA和长期EMA交叉确认趋势,减少虚假突破

- 动态通道宽度:根据趋势强度动态调整ATR乘数,在强趋势中使用更紧的通道获取更早的信号

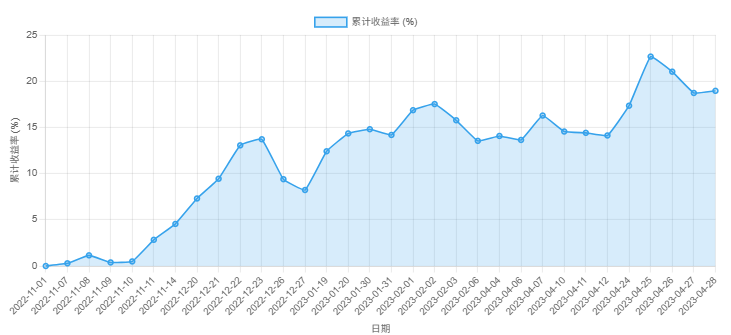

回测

回测初始设置

- 测试周期: 2022 年 11 月 1 日 - 2023 年 4 月 30 日

- 交易品种: CFFEX.IC2306

- 初始资金: 1000万元

回测结果

上述回测累计收益走势图

代码

#!/usr/bin/env python # -*- coding: utf-8 -*- __author__ = "Chaos" from tqsdk import TqApi, TqAuth, TqBacktest, TargetPosTask, BacktestFinished from datetime import date import numpy as np import pandas as pd # ===== 全局参数设置 ===== SYMBOL = "CFFEX.IC2306" # 中证500指数期货合约 POSITION_SIZE = 30 # 持仓手数(黄金的合适仓位) START_DATE = date(2022, 11, 1) # 回测开始日期 END_DATE = date(2023, 4, 30) # 回测结束日期 # Keltner Channel参数 EMA_PERIOD = 8 # EMA周期 ATR_PERIOD = 7 # ATR周期 ATR_MULTIPLIER = 1.5 # ATR乘数 # 新增参数 - 趋势确认与止损 SHORT_EMA_PERIOD = 5 # 短期EMA用于趋势确认 STOP_LOSS_PCT = 0.8 # 止损百分比(相对于ATR) TRAILING_STOP = True # 使用移动止损 print(f"开始回测 {SYMBOL} 的Keltner Channel策略...") print(f"参数: EMA周期={EMA_PERIOD}, ATR周期={ATR_PERIOD}, ATR乘数={ATR_MULTIPLIER}") print(f"额外参数: 短期EMA={SHORT_EMA_PERIOD}, 止损参数={STOP_LOSS_PCT}ATR, 移动止损={TRAILING_STOP}") try: api = TqApi(backtest=TqBacktest(start_dt=START_DATE, end_dt=END_DATE), auth=TqAuth("快期账号", "快期密码")) # 订阅K线数据 klines = api.get_kline_serial(SYMBOL, 60 * 60 * 24) # 日K线 # 订阅行情获取交易时间 quote = api.get_quote(SYMBOL) target_pos = TargetPosTask(api, SYMBOL) # 初始化交易状态 position = 0 # 当前持仓 entry_price = 0 # 入场价格 stop_loss = 0 # 止损价格 high_since_entry = 0 # 入场后的最高价(用于移动止损) low_since_entry = 0 # 入场后的最低价(用于移动止损) trend_strength = 0 # 趋势强度 # 记录交易信息 trades = [] while True: api.wait_update() if api.is_changing(klines): # 确保有足够的数据 if len(klines) < max(EMA_PERIOD, ATR_PERIOD, SHORT_EMA_PERIOD) + 1: continue # 计算指标 close = klines.close.values high = klines.high.values low = klines.low.values # 计算中轨(EMA)和短期EMA(用于趋势确认) ema = pd.Series(close).ewm(span=EMA_PERIOD, adjust=False).mean().values ema_short = pd.Series(close).ewm(span=SHORT_EMA_PERIOD, adjust=False).mean().values # 计算趋势方向和强度 trend_direction = 1 if ema_short[-1] > ema[-1] else -1 if ema_short[-1] < ema[-1] else 0 trend_strength = abs(ema_short[-1] - ema[-1]) / close[-1] * 100 # 趋势强度百分比 # 计算ATR tr = np.maximum(high - low, np.maximum( np.abs(high - np.roll(close, 1)), np.abs(low - np.roll(close, 1)) )) atr = pd.Series(tr).rolling(ATR_PERIOD).mean().values current_atr = float(atr[-1]) # 动态调整ATR乘数,根据趋势强度调整通道宽度 dynamic_multiplier = ATR_MULTIPLIER if trend_strength > 0.5: # 强趋势时使用更窄的通道 dynamic_multiplier = ATR_MULTIPLIER * 0.8 # 计算通道上下轨 upper_band = ema + dynamic_multiplier * atr lower_band = ema - dynamic_multiplier * atr # 获取当前价格和指标值 current_price = float(close[-1]) current_upper = float(upper_band[-1]) current_lower = float(lower_band[-1]) current_ema = float(ema[-1]) current_time = quote.datetime # 使用quote的datetime获取当前时间 # 更新入场后的最高/最低价 if position > 0: high_since_entry = max(high_since_entry, current_price) # 更新移动止损 if TRAILING_STOP and high_since_entry > entry_price: trailing_stop = high_since_entry * (1 - STOP_LOSS_PCT * current_atr / current_price) stop_loss = max(stop_loss, trailing_stop) elif position < 0: low_since_entry = min(low_since_entry, current_price) # 更新移动止损 if TRAILING_STOP and low_since_entry < entry_price: trailing_stop = low_since_entry * (1 + STOP_LOSS_PCT * current_atr / current_price) stop_loss = min(stop_loss if stop_loss > 0 else float('inf'), trailing_stop) # 交易逻辑 if position == 0: # 空仓 # 确认趋势方向并突破通道 if current_price > current_upper and trend_direction > 0: # 增加成交量过滤 position = POSITION_SIZE entry_price = current_price high_since_entry = current_price low_since_entry = current_price # 设置初始止损 stop_loss = current_price * (1 - STOP_LOSS_PCT * current_atr / current_price) target_pos.set_target_volume(position) print(f"开多仓: 价格={current_price:.2f}, 上轨={current_upper:.2f}, 止损={stop_loss:.2f}") trades.append(("开多", current_time, current_price)) elif current_price < current_lower and trend_direction < 0: position = -POSITION_SIZE entry_price = current_price high_since_entry = current_price low_since_entry = current_price # 设置初始止损 stop_loss = current_price * (1 + STOP_LOSS_PCT * current_atr / current_price) target_pos.set_target_volume(position) print(f"开空仓: 价格={current_price:.2f}, 下轨={current_lower:.2f}, 止损={stop_loss:.2f}") trades.append(("开空", current_time, current_price)) elif position > 0: # 持有多头 # 止损、回落到中轨或趋势转向时平仓 if (current_price <= stop_loss or current_price <= current_ema or (current_price < current_lower and trend_direction < 0)): profit_pct = (current_price / entry_price - 1) * 100 profit_points = current_price - entry_price target_pos.set_target_volume(0) print(f"平多仓: 价格={current_price:.2f}, 盈亏={profit_pct:.2f}%, {profit_points:.2f}点") position = 0 entry_price = 0 stop_loss = 0 trades.append(("平多", current_time, current_price)) elif position < 0: # 持有空头 # 止损、回升到中轨或趋势转向时平仓 if (current_price >= stop_loss or current_price >= current_ema or (current_price > current_upper and trend_direction > 0)): profit_pct = (entry_price / current_price - 1) * 100 profit_points = entry_price - current_price target_pos.set_target_volume(0) print(f"平空仓: 价格={current_price:.2f}, 盈亏={profit_pct:.2f}%, {profit_points:.2f}点") position = 0 entry_price = 0 stop_loss = 0 trades.append(("平空", current_time, current_price)) except BacktestFinished as e: print(f"回测完成: {e}")